Today I saw an article on Hacker News entitled, “America’s CEOs Want You to Work Until You’re 70”. I was particularly surprised by this article appearing out of the blue because I take it for granted that America will eventually have to raise the retirement age to avoid bankruptcy. After reading the article, I wasn’t able to figure out why the story had been run at all. So I decided to do some basic fact-checking.

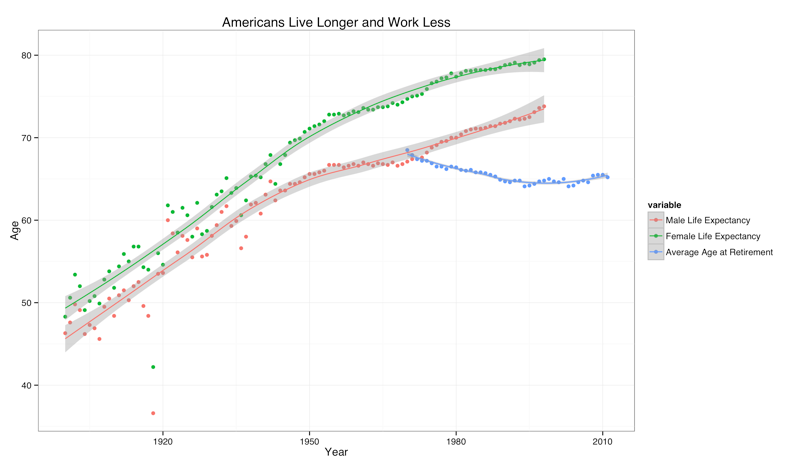

I tracked down some time series data about life expectancies in the U.S. from Berkeley and then found some time series data about the average age at retirement from the OECD. Plotting just these two bits of information, as shown below, makes it clear that Americans are spending a larger proportion of their life in retirement.

Perhaps I’m just naive, but it seems obvious to me that we can’t afford to take on several additional years of retirement pension liabilities for every living American. If Americans are living longer, we will need them to work longer in order to pay our bills.